Summary

In the ECB’s Survey of Professional Forecasters (SPF) for the fourth quarter of 2023, expectations for headline HICP inflation were broadly unchanged compared to the previous survey (conducted in the third quarter), while those for HICP inflation excluding energy and food (HICPX) were revised downward.[1] Based on respondents’ qualitative information, this difference mainly reflects the impact of higher oil prices on the energy component. Headline inflation was expected to decline from 5.6% in 2023 to 2.7% in 2024 and 2.1% in 2025. Longer-term HICP inflation expectations (for 2028) were unchanged at 2.1%, but the uncertainty surrounding them remained at elevated levels. Real GDP growth expectations were revised down for 2023 and 2024 but were unchanged for 2025. The downward revision for 2024 mainly reflected a carry-over from lower expected quarter-on-quarter growth for the third and fourth quarters of 2023. The balance of risks to the growth outlook remained tilted to the downside. Longer-term GDP growth expectations were unchanged at 1.3%. Unemployment expectations were around 6.5-6.7% for 2023 to 2025 and 6.5% for 2028. Compared with the previous survey round, notwithstanding the lower growth expectations, the profile of unemployment rate expectations was marginally lower.

Table 1

Results of the SPF in comparison with other expectations and projections

(annual percentage changes, unless otherwise indicated)

Survey horizon | ||||

|---|---|---|---|---|

2023 | 2024 | 2025 | Longer term1) | |

HICP inflation | ||||

Q4 2023 SPF | 5.6 | 2.7 | 2.1 | 2.1 |

Previous SPF (Q3 2023) | 5.5 | 2.7 | 2.2 | 2.1 |

ECB staff macroeconomic projections (September 2023) | 5.6 | 3.2 | 2.1 | - |

Consensus Economics (October 2023) | 5.6 | 2.5 | 1.9 | 2.1 |

Memo: HICP inflation excluding energy, food, alcohol and tobacco | ||||

Q4 2023 SPF | 5.1 | 2.9 | 2.2 | 2.0 |

Previous SPF (Q3 2023) | 5.1 | 3.1 | 2.3 | 2.1 |

ECB staff macroeconomic projections (September 2023) | 5.1 | 2.9 | 2.2 | - |

Consensus Economics (October 2023) | 5.0 | 2.7 | - | - |

Real GDP growth | ||||

Q4 2023 SPF | 0.5 | 0.9 | 1.5 | 1.3 |

Previous SPF (Q3 2023) | 0.6 | 1.1 | 1.5 | 1.3 |

ECB staff macroeconomic projections (September 2023) | 0.7 | 1.0 | 1.5 | - |

Consensus Economics (October 2023) | 0.5 | 0.6 | 1.4 | 1.3 |

Unemployment rate2) | ||||

Q4 2023 SPF | 6.5 | 6.7 | 6.6 | 6.5 |

Previous SPF (Q3 2023) | 6.6 | 6.7 | 6.7 | 6.5 |

ECB staff macroeconomic projections (September 2023) | 6.5 | 6.7 | 6.7 | - |

Consensus Economics (October 2023) | 6.5 | 6.7 | - | - |

1) Longer-term expectations refer to 2028.

2) As a percentage of the labour force.

1 Counterbalancing revisions to HICP inflation expectations for 2023-25

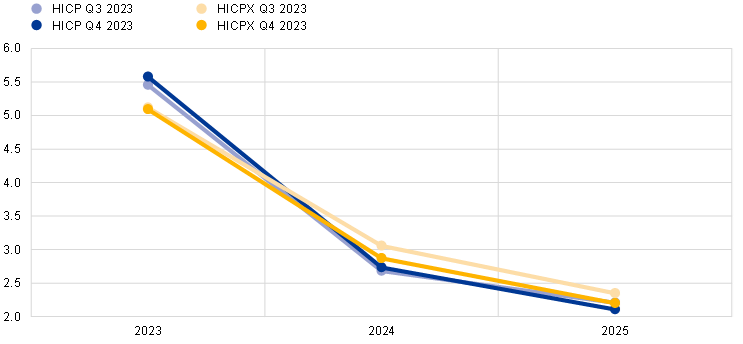

SPF respondents made limited counterbalancing revisions to their HICP inflation expectations for 2023 to 2025. Inflation expectations for 2023 were revised upward by 0.1 percentage points to 5.6%, those for 2024 were unchanged, while those for 2025 were revised downward by 0.1 percentage points to 2.1% (see Chart 1). Respondents’ qualitative explanations suggest that the upward revision for 2023 was mainly due to higher oil prices. Compared with the September 2023 ECB staff macroeconomic projections, inflation expectations in this SPF round were exactly the same for 2023 and 2025 but substantially lower – by 0.5 percentage points – for 2024 (see Table 1).

Chart 1

Inflation expectations: overall HICP inflation and HICP inflation excluding energy and food

(annual percentage changes)

SPF expectations for inflation excluding energy and food were revised down for 2024 and 2025. HICPX expectations for 2023, 2024 and 2025 stood at 5.1%, 2.9% and 2.2% respectively – representing no change for 2023 but downward revisions of 0.2 percentage points for 2024 and 0.1 percentage points for 2025. Respondents indicated that the downward revisions reflected a weaker economic situation and the impact of monetary policy tightening (both for the euro area and globally). Respondents expected a notable moderation in non-energy industrial goods inflation, driven by an easing of supply pressures, the abating of indirect effects from past energy hikes and declines in some non-labour input costs. On the other hand, they considered that services inflation would remain higher and more persistent than goods inflation – mainly reflecting wage pressures. The downward revisions to the HICPX expectations bring them exactly into line with the projections in the September 2023 ECB staff macroeconomic projections (see Table 1).

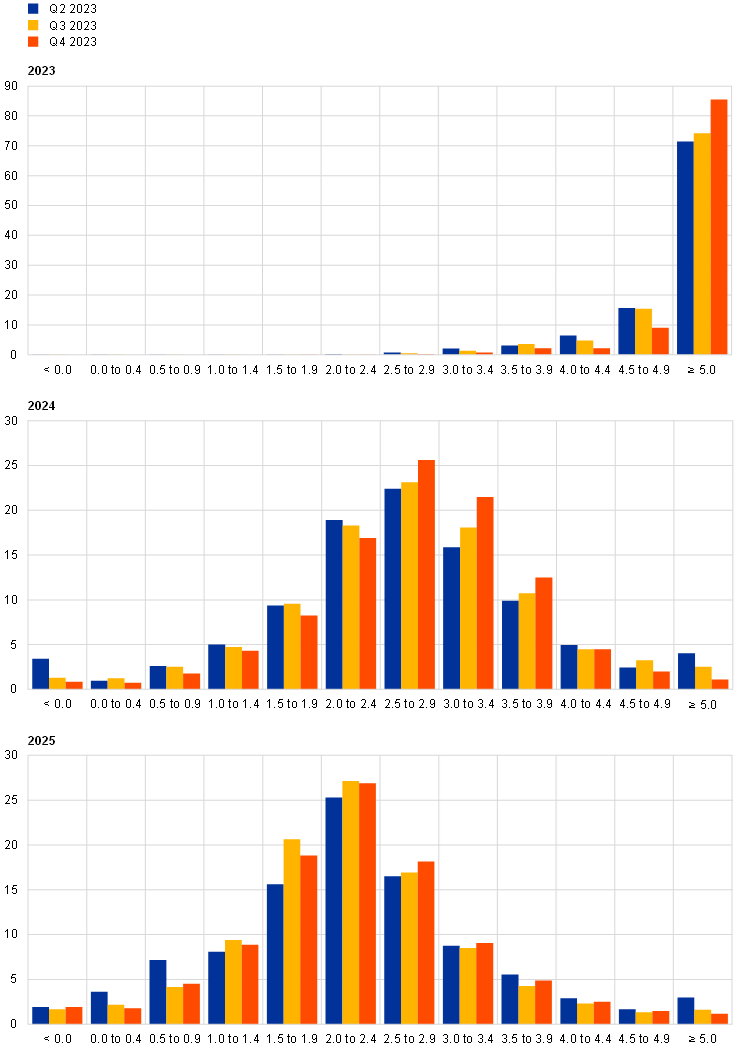

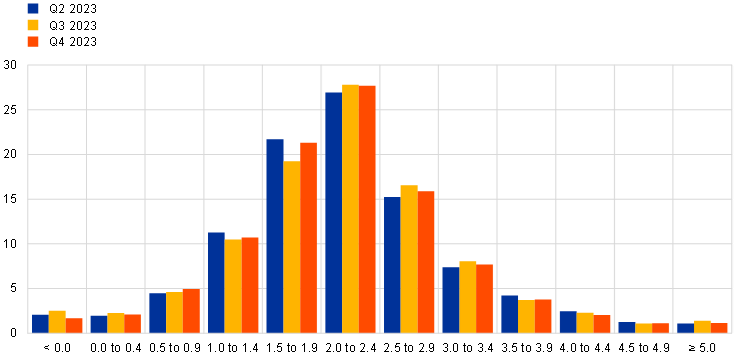

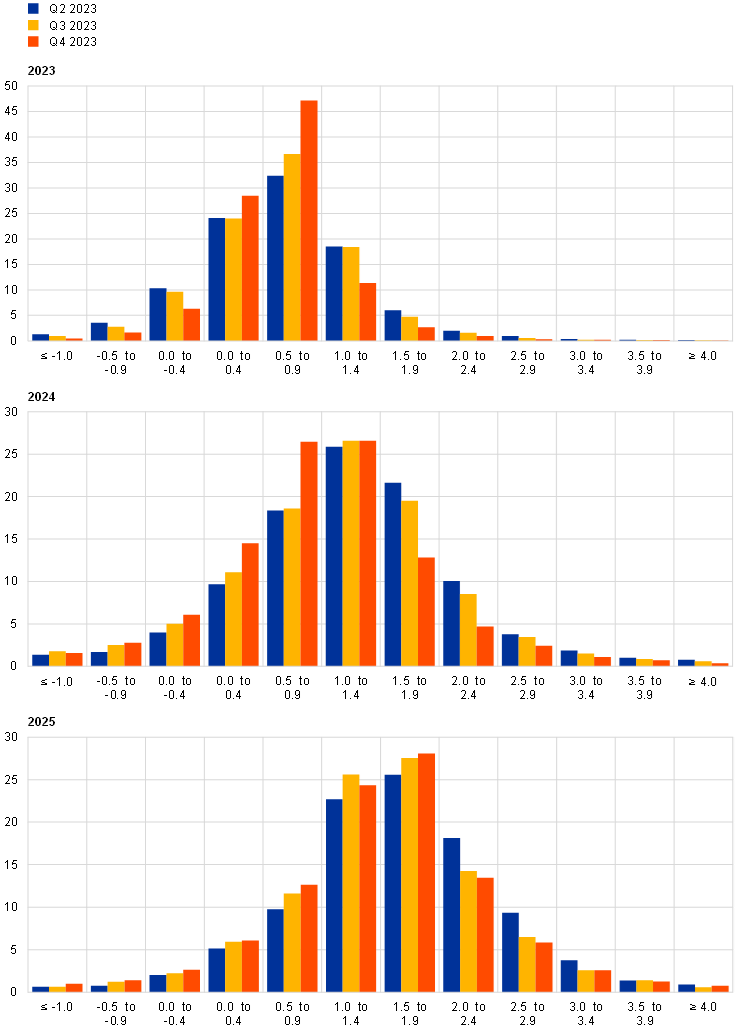

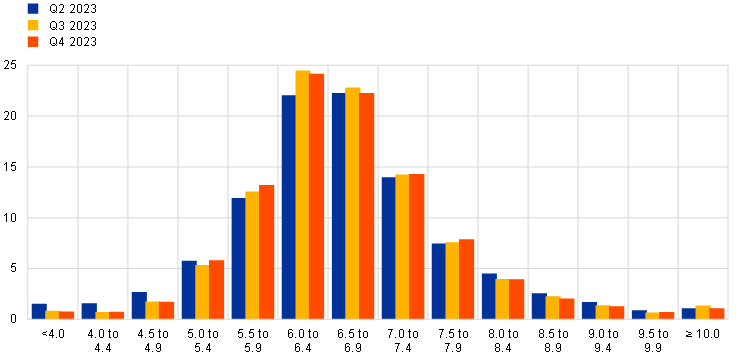

Quantitative indicators of uncertainty surrounding the short and medium-term inflation outlook remained unchanged at elevated levels, while the balance of risks moved more to the upside.[2] The high level of “aggregate uncertainty” (the standard deviation of the aggregate probability distribution) stemmed from a combination of a high average level of “individual uncertainty” (measured by the average width of the individual probability distributions) and substantial “disagreement” across forecasters about their point forecasts (measured as the standard deviation of the individual point forecasts). Aggregate probability distributions for the calendar years from 2023 to 2025 are presented in Chart 2. The balance-of-risk indicator for the two-years-ahead horizon moved further to the upside, but the risk associated with very high outcomes decreased (the weight of outcomes of inflation being 5% or higher decreased to 1.4%, compared to 6.8% a year ago in the fourth quarter of 2022 survey round). According to the qualitative remarks, the main upside risks relate to energy prices and possible wage developments from second-round effects.

Chart 2

Aggregate probability distributions for expected inflation in 2023, 2024 and 2025

(x-axis: HICP inflation expectations, annual percentage changes; y-axis: probability, percentages)

Notes: The SPF asks respondents to report their point forecasts and to separately assign probabilities to different ranges of outcomes. This chart shows the average probabilities assigned to different ranges of inflation outcomes in 2023, 2024 and 2025. To minimise the number of bins in the questionnaire, the upper bin for inflation outcomes was set at ≥ 5.0%. The fact that this would lead to most probability being assigned to the upper bin for some horizons was flagged to respondents when sending out the questionnaire.

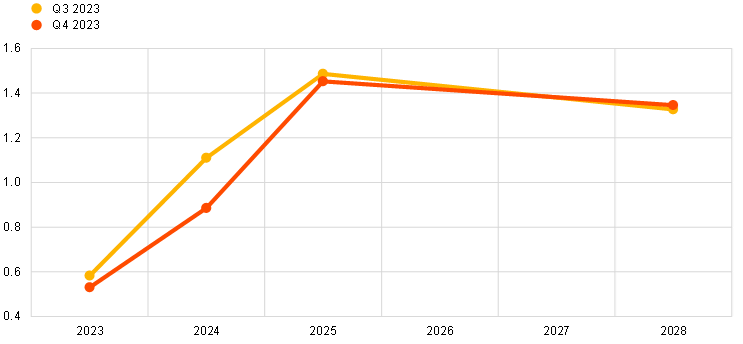

2 Longer-term inflation expectations unchanged

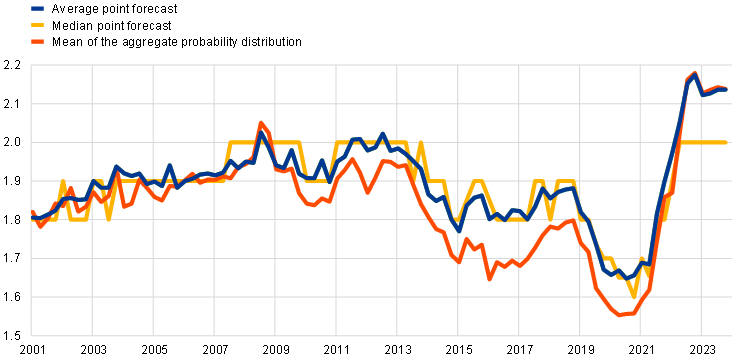

Longer-term inflation expectations (which relate to 2028) were unchanged at 2.1%. Thus, after having moved up noticeably since the third quarter of 2021, there are increasing signs that longer-term inflation expectations in the SPF have levelled off since the fourth quarter of 2022 at around 2.1%. This also holds when excluding the two highest and two lowest responses. The median and modal point expectations were unchanged at 2.0%, while the estimated mean of the aggregate probability distribution was unchanged at 2.1% (see Chart 3). In the last three survey rounds there has been a drop in the number of respondents reporting longer-term inflation expectations of below 1.9%. The distribution of longer-term point inflation expectations has become much more focused on 2.0%, and expectations of inflation lower than 2% have subsided significantly (see Chart 4).

Chart 3

Longer-term inflation expectations

(annual percentage changes)

Chart 4

Distribution of point expectations for HICP inflation in the longer term

(x-axis: longer-term HICP inflation expectations, annual percentage changes; y-axis: percentages of respondents)

Notes: The SPF asks respondents to report their point forecasts and to separately assign probabilities to different ranges of outcomes. This chart shows the spread of point forecast responses. In the SPF rounds in the third and fourth quarters of 2023, longer-term expectations refer to 2028. In the second quarter of 2023 survey round they referred to 2027.

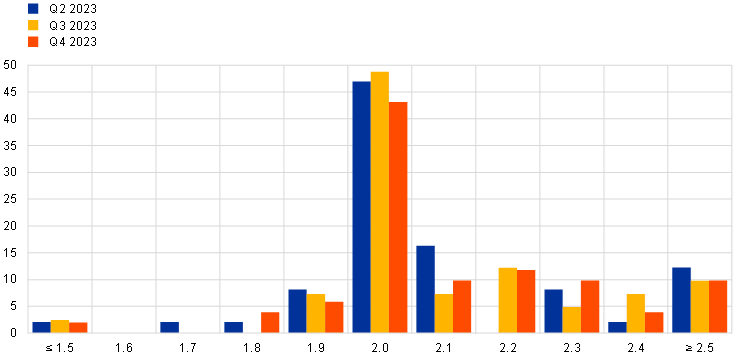

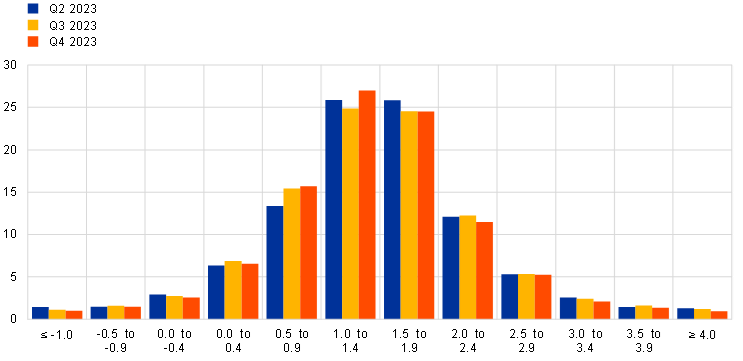

Uncertainty surrounding longer-term inflation expectations eased somewhat (albeit remaining at elevated levels), while the balance of risks remained broadly neutral. The high level of “aggregate uncertainty” (see Chart 5) stemmed from a combination of elevated “disagreement” and heightened “individual uncertainty”. The balance-of-risk indicator remained close to zero (i.e. neutral). The probability of longer-term inflation being in the range 1.5-2.5% increased slightly to 49%, from 47% in the previous survey round, while there were small reductions in the probabilities either side of this range.

Chart 5

Aggregate probability distribution for longer-term inflation expectations

(x-axis: HICP inflation expectations, annual percentage changes; y-axis: probability, percentages)

Notes: The SPF asks respondents to report their point forecasts and to separately assign probabilities to different ranges of outcomes. This chart shows the average probabilities assigned to different ranges of inflation outcomes in the longer term. In the SPF rounds in the third and fourth quarters of 2023, longer-term expectations refer to 2028. In the second quarter of 2023 survey round they referred to 2027.

The mean longer-term expectations for HICP inflation excluding energy and food (HICPX) declined 0.1 percentage points to 2.0%.[3] The median and modal longer-term point expectations for HICPX inflation were unchanged at 2.0%. Broadly speaking, since the fourth quarter of 2016 (when respondents were first asked about their expectations for HICPX inflation) the evolution of longer-term expectations for HICP inflation and HICPX inflation has been similar, with a difference in levels of around 0.1 percentage points on average. This gap narrowed in the previous survey round (third quarter of 2023), but that narrowing was reversed in this round. A similar narrowing and reversal was seen in the survey rounds for the third and fourth quarters of 2022.

3 Real GDP growth expectations slightly down for 2023 and 2024

GDP growth expectations in the fourth quarter of 2023 survey round stood at 0.5% for 2023, 0.9% for 2024 and 1.5% for 2025 (see Chart 6). The outlooks for 2023 and 2024 were revised downward by 0.1 and 0.2 percentage points respectively, while expectations for 2025 were unchanged compared to the previous round. The narrative of respondents related to the growth profile did not change significantly. Higher wage growth and declining headline inflation were still expected to boost real household income and support household spending. However, this impact on growth was expected to be partly offset by the impact of tighter monetary conditions and continued uncertainty about further tightening associated with persistence in core inflation and the recent rise in oil prices. Continued weaker growth globally, trade tensions and weakening fiscal support were seen as major downside risks to euro area growth. Longer-term growth expectations (referring to 2028) were 1.3%, the same level as in the previous survey round.

Chart 6

Expectations for real GDP growth

(annual percentage changes)

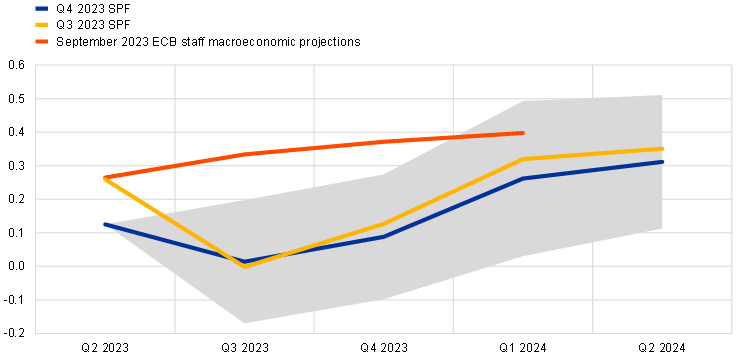

Respondents’ short-term GDP outlook implies a sluggish second half of 2023, with economic activity picking up over the first half of 2024.[4] Actual quarter-on-quarter real GDP growth for the second quarter of 2023 was 0.1%, which was lower than the forecast of 0.3% in the previous SPF round. In the latest survey round, forecasters expect a profile for quarter-on-quarter GDP growth for the period between the third quarter of 2023 and the second quarter of 2024 very similar to, albeit slightly lower than, the September 2023 ECB staff macroeconomic projections (see Chart 7). The share of respondents expecting at least one quarter of negative growth over the next four quarters rose to 42%, from 23% in the previous survey round, while 6% (previously 7%) forecast a technical recession (i.e. two consecutive quarters of negative growth) over the same period.

Chart 7

Expected profile of quarter-on-quarter GDP growth

(quarter-on-quarter percentage changes)

Note: The grey area indicates one standard deviation (of individual expectations) around average SPF expectations.

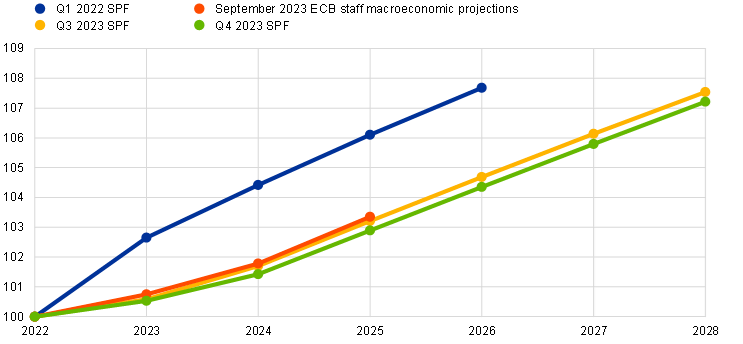

The level of economic activity implied by the growth expectations has been revised down only slightly compared to the previous survey round, but it still remains substantially below the level implied by growth expectations prior to Russia’s invasion of Ukraine. Compared to the SPF round for the first quarter of 2022 (conducted in early January, before the invasion of Ukraine), the implied level of real GDP for 2026 is about 3.1% lower (see Chart 8). For 2024 and 2025 it is only marginally lower (by 0.1% and 0.2% respectively) than real GDP implied by the September 2023 ECB staff macroeconomic projections.

Chart 8

Forecast profile of real GDP

(index: 2022 = 100)

Note: Growth expectations for years not surveyed have been interpolated linearly.

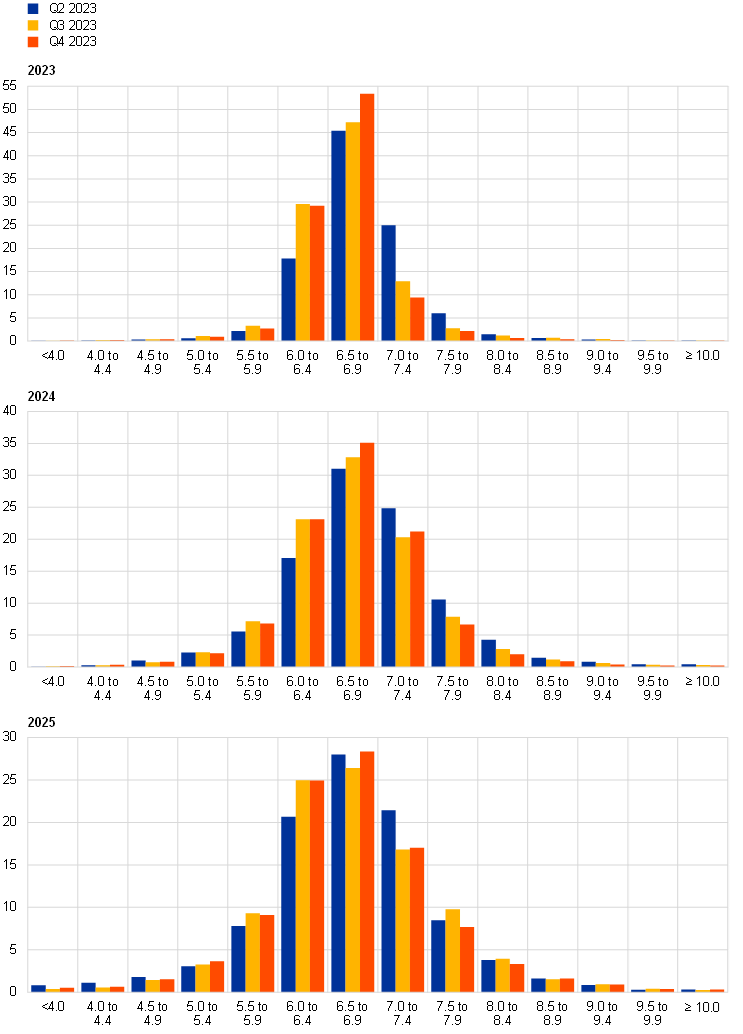

While uncertainty about the growth outlook eased slightly, it remained at elevated levels (see Chart 9 and Chart 10). Aggregate uncertainty was unchanged at the two-years-ahead horizon and declined slightly at the longer horizon, remaining in both cases above the levels prevailing prior to the coronavirus (COVID-19) pandemic but considerably lower than the peaks reached in 2020. After a substantial fall in the previous survey round, the balance of risks for the two-years-ahead horizon rose only slightly, staying below zero (i.e. to the downside). For the longer horizon, it remained positive, but lower than in the previous survey round.

Chart 9

Aggregate probability distributions for GDP growth expectations for 2023, 2024 and 2025

(x-axis: real GDP growth expectations, annual percentage changes; y-axis: probability, percentages)

Notes: The SPF asks respondents to report their point forecasts and to separately assign probabilities to different ranges of outcomes. This chart shows the average probabilities assigned to different ranges of real GDP growth outcomes in 2023, 2024 and 2025.

Chart 10

Aggregate probability distributions for longer-term GDP growth expectations

(x-axis: real GDP growth expectations, annual percentage changes; y-axis: probability, percentages)

Notes: The SPF asks respondents to report their point forecasts and to separately assign probabilities to different ranges of outcomes. This chart shows the average probabilities assigned to different ranges of real GDP growth outcomes in the longer term. In the SPF rounds in the third and fourth quarters of 2023, longer-term expectations refer to 2028. In the second quarter of 2023 survey round they referred to 2027.

4 Profile of unemployment rate expectations slightly down

In the fourth quarter of 2023, respondents expected unemployment rates of 6.5%, 6.7% and 6.6% for 2023, 2024 and 2025 respectively. The profile of the unemployment rate expectations has been revised slightly downward over the entire horizon by around 0.1 percentage points compared to the previous survey round. The expectation for longer-term unemployment (2028) was 6.5%, unchanged from the previous round. Similar to the trajectory of the previous round, the numbers imply that the unemployment rate is expected to increase over the rest of 2023 and into 2024, peaking at a lower level than expected in the previous survey round, and then gradually decrease over the rest of the horizon (see Chart 11). The slight downward revision is explained by a surprisingly resilient labour market relative to real economic conditions and the economic cycle – with some respondents referring to labour hoarding decisions of firms owing to labour shortages. Despite this resilience, respondents still expect some increase in the unemployment rate given the monetary tightening, weak growth outlook and indications of loosening labour market tightness. Unemployment is still expected to fall in the longer term, primarily owing to demographic factors.

Chart 11

Expectations for the unemployment rate

(percentages of the labour force)

The level of uncertainty regarding short and longer-term unemployment rate expectations remained at relatively high levels. Aggregate uncertainty has fluctuated around elevated levels (higher than those prevailing before the pandemic) in recent survey rounds. Regarding risks, respondents noted primarily upside risks to the unemployment outlook amid the weak outlook for growth and possible reductions in the degree of labour hoarding (see Chart 12 and Chart 13).

Chart 12

Aggregate probability distributions for the unemployment rate in 2023, 2024 and 2025

(x-axis: unemployment rate expectations, percentages of the labour force; y-axis: probability, percentages)

Notes: The SPF asks respondents to report their point forecasts and to separately assign probabilities to different ranges of outcomes. This chart shows the average probabilities assigned to different ranges of unemployment rate outcomes for 2023, 2024 and 2025.

Chart 13

Aggregate probability distribution for the unemployment rate in the longer term

(x-axis: unemployment rate expectations, percentages of the labour force; y-axis: probability, percentages)

Notes: The SPF asks respondents to report their point forecasts and to separately assign probabilities to different ranges of outcomes. This chart shows the average probabilities assigned to different ranges of unemployment rate outcomes in the longer term. In the SPF rounds in the third and fourth quarters of 2023, longer-term expectations refer to 2028. In the second quarter of 2023 survey round they referred to 2027.

5 Expectations for other variables

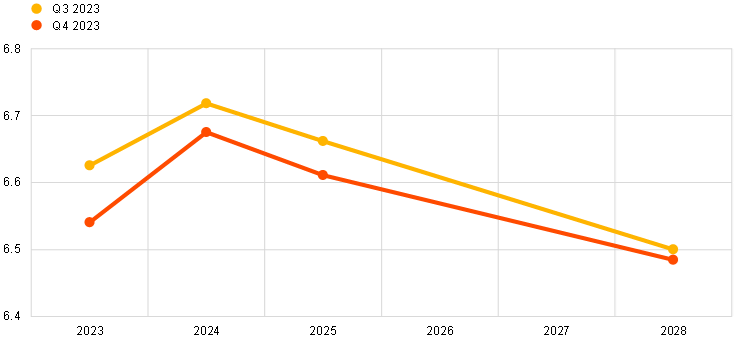

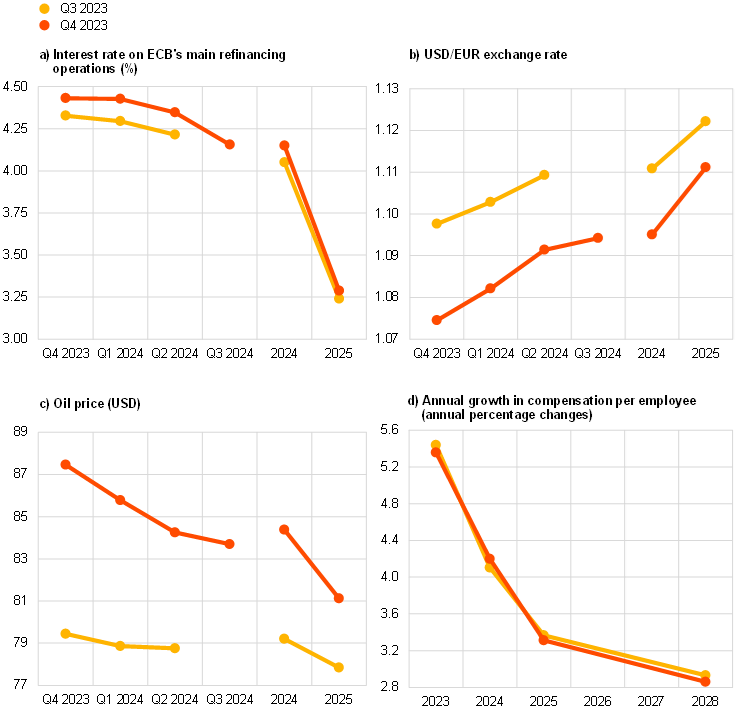

Forecasters expected the rate on the ECB’s main refinancing operations (MROs) to remain at 4.5% before easing slightly in the latter part of 2024 and falling further to 3.25% in 2025. They expected the euro to marginally appreciate against the US dollar, from USD 1.07 in the fourth quarter of 2023 to USD 1.11 in 2025, and oil prices to fall gradually from USD 87 per barrel to USD 81 per barrel. And they expected nominal wages to increase by 5.4% in 2023, but then to moderate to a growth rate of 4.2% in 2024, 3.3% in 2025 and 2.9% in the longer term.

Respondents expected the ECB’s MRO interest rate to remain at 4.5% in the fourth quarter of 2023. They expected it to remain at this level until the second or third quarter of 2024, after which they expected some decline before rates fall further to 3.25% in 2025 (see Chart 14a). While the mean expectation was 4.43% for the fourth quarter of 2024, most respondents still expected rates to be maintained at 4.5%. Compared with the previous survey round, the profile was revised upward by around 0.1 percentage points, but with a slightly more modest upward revision for 2025.

On average, the USD/EUR exchange rate was expected to rise from 1.07 in the fourth quarter of 2023 to 1.11 in 2025 (see Chart 14b). The profile follows a similar trajectory to the previous survey round, but was revised downwards.

Compared with the previous round, the expected level of US dollar-denominated oil prices was revised upward over the entire horizon. Prices for the fourth quarter of 2023 were revised upwards to USD 87 per barrel from USD 79 per barrel. Thereafter, oil prices are expected to follow a slightly steeper decline than expected in the previous round but to remain at higher levels (USD 5 higher for 2024 and USD 3 higher for 2025) (see Chart 14c).

Expectations for annual growth in compensation per employee were broadly unchanged at 5.4% for 2023, up 0.1 percentage points at 4.2% for 2024 and down 0.1 percentage points at 3.3% for 2025. For the longer term, expectations were unchanged at 2.9% (see Chart 14d).

Chart 14

Expectations for other variables

Annex (chart data)

Excel data for all charts can be downloaded here.

© European Central Bank, 2023

Postal address 60640 Frankfurt am Main, Germany

Telephone +49 69 1344 0

Website www.ecb.europa.eu

All rights reserved. Reproduction for educational and non-commercial purposes is permitted provided that the source is acknowledged.

For specific terminology please refer to the ECB glossary (available in English only).

PDF ISBN 978-92-899-5810-3, ISSN 2363-3670, doi:10.2866/360036, QB-BR-23-004-EN-N

HTML ISBN 978-92-899-5811-0, ISSN 2363-3670, doi:10.2866/120084, QB-BR-23-004-EN-Q

The survey was conducted between 29 September and 5 October 2023, with 63 responses received. This is above the historical average for the response rate in rounds conducted in the fourth quarter of the year. Participants were provided with a common set of the latest available data for annual HICP inflation (September 2023 flash estimates: overall inflation, 4.3%; underlying inflation, 4.5%), annual GDP growth (second quarter of 2023, 0.5%) and unemployment (August 2023, 6.4%). This report was drafted on the basis of data available on 13 October 2023.

The width of the reported probability distributions indicates the perceived degree of overall uncertainty, whereas the asymmetry of the distributions indicates whether that uncertainty is more concentrated on higher or lower outturns – i.e. it measures the perceived balance of risks. As regards uncertainty, it can be shown that the width (or standard deviation) of the aggregate probability distribution (i.e. “aggregate uncertainty”) is a function of the average width (or standard deviation) of the individual probability distributions (i.e. “individual uncertainty”) and the standard deviation of the individual point forecasts (i.e. “disagreement”).

Of the 28 respondents who provided longer-term HICPX expectations in both the third and fourth quarters of 2023, 22 made no changes to their forecasts, one revised them up and five revised them down.

Based on data from 48 respondents.

- 27 October 2023