Risk and the Macro-economy

Keynote address by Jean-Claude Trichet, President of the ECB at the conference ‘The ECB and its Watchers X’Frankfurt am Main, 5 September 2008

Ladies and gentlemen,

After an extended period of ample financial market liquidity and exceptionally low rewards for risk, the loss in the value of important classes of real assets has imparted a sharp deterioration in investor appetite. Rises in commodity prices, by eroding consumers’ purchasing power and real income prospects, have reinforced households’ risk aversion.

A long phase of heightened risk tolerance in our economies has come to an end. To the extent that the more recent turns in the markets correct past excesses, this is a welcome – if painful – process that we had anticipated and asked market participants to prepare for in past interventions.

At the same time, the decline in the compensation for risk that the recent turmoil has partly reversed is not a recent development. It started a quarter of a century ago, in tandem with – and probably reflecting – what seems to have been a persistent decline in macroeconomic uncertainty. So, to the extent that this moderation in macroeconomic fluctuations – in aggregate risk – would be confirmed as a permanent acquisition of modern economies, there is some reason to believe that the trend to lower risk valuations – beyond the needed corrections of the more recent excesses – could in the end reassert itself.

In this talk I will reflect upon some evidence that lies at the heart of the mechanisms through which risk valuation makes contact with real economic decisions. The ultimate aim of my reflections is to find hints about the fundamental value of risk.

Theories, for which I have some sympathy, have it that there is a historical break in risk valuation in the markets, and the realisation of that break largely mirrors structural developments in the balance between savings and investment on a global scale. China’s phenomenal growth in domestic manufacturing capacity and income production was not matched by an equi-proportional growth in domestic spending capacity – so Chinese savings grew ahead of even the dramatic pace at which domestic investment has expanded. At the same time, the aftermaths of the East Asian crisis brought about an “investment strike” in many economies bordering on the Asian Pacific, and taught authorities in those countries that bigger liquidity buffers – denominated in safe Western currencies – were needed to defend themselves against the volatile behaviour of foreign private investors. Finally, international financial markets were called upon – once again – to recycle the massive hard-currency balances that were being accumulated by commodity exporting countries. All this has made saving – and wealth – abundant ex ante relative to investment and income. And has led to a downside adjustment in the rewards that investors can claim to receive in compensation for their finance.

These developments at time have dominated the financial landscape. But the breaks in the evolution of the market rewards for risk on which I will focus date long before the rise of the Asian economies and the increase in commodity prices. So, I will search for a fundamental connection between financial risk and macroeconomic performance in the developed countries, which will be the focus of my remarks. What is the direction of this link? Does the Great Moderation determine the quantum of risk traded in the markets? Or does the price of risk determined in the financial markets contribute and partly determine those fluctuations? And what is structural in this link – and thus likely to persist beyond short-term volatilities – and what is transient?

A complete understanding of these relations would bring invaluable insights for policy considerations. For one thing, the centrepiece of dynamic macroeconomics is the equation of savings to investment. Asset prices – and the risk remuneration that they embody – are the mechanisms that do all this equating. Therefore, sustained movements in risk premia of the size that we have seen in the past quarter of a century are bound to have important implications for the allocation of consumption and investment across times and states of nature, and for the determination of aggregate demand at any point in time and in any economic state. I will also mention new – to some extent unknown – forms of interactions between financial markets and the real economy.

One possibility that many observers have contemplated is that the prices determined in the market for key factors of production – such as energy or other commodities – might be increasingly influenced by forces and trading strategies that are motivated by the financial drive toward portfolio diversification, beside the desire to secure access to a physical delivery. Again, the way these markets might be pricing financial risk might make the interpretation of those prices more difficult.

Unfortunately, my conclusion is that the state of our knowledge is not advanced enough to draw definitive conclusions about the nature and the directions of influences between risk pricing and the macro-economy. I will nevertheless submit my conjectures and lay out some basic behavioural principles that could help policymakers minimise major losses amid the uncertainty surrounding the current economic juncture.

I also appeal to the many distinguished scholars that sit in front of me today to concentrate their minds to elucidate these relations.

1. Risk premia and macroeconomic conditions

There is no univocal way to assess whether asset values are high or low relative to economic norms. Popular commentary often focuses on price indices and how they deviate from long-term averages. But, of course, index levels can vary because of general price inflation, or growth in the real economy, or changes in the size of publicly traded assets relative to the economy. So, it is customary for analysts to scale asset prices in various ways.

A summary statistic of valuations that abstracts from scaling problems is the “asset risk premium”, or the rate of excess return investors expect to earn over the long run from their investment at current prices. [1] If the asset generates uncertain payoffs, investors ask to be compensated for this risk, which they would not bear if they chose to hold a competiting security with comparatively more predictable returns. The risk premium represents this reward. For a given stream of expected cash flows, a higher risk premium today signals a diminished willingness to hold the risky asset or, equivalently, a higher required return for doing so. Higher returns can be generated only by future price appreciation from a lower current price. So, an increase in the premium today is associated with a capital loss in the form of a drop in the current price of the asset. Conversely, a low premium signals a high current price relative to the expected income stream discounted at the risk-free rate.

The risk premium measures the attractiveness of a risky investment relative to risk-free alternatives. Indirectly, it is a measure of the market’s appetite for investment risk.

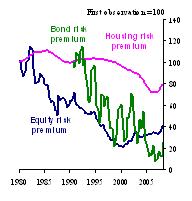

These figures [Figures 1a, 2a and 3] document the basic facts that constitute the subject of my considerations on the risk and the macro-economy. I focus here on estimates of the risk premia paid on four important asset classes: equity, houses, government bonds and corporate credit securities. They span the four markets for external finance that are most critical to the functioning of modern economies: the market for capital, installed in businesses and in residential establishments, and the market for credit, to government and corporate borrowers. I use US and euro area observations, whenever these are available, but international evidence broadly confirms this picture. And I concentrate on the last quarter of a century when the movements which I shall reflect upon are most evident.

What do we see in these pictures? Two things: First, if I emphasise trends rather than waves, I see that risk premia on a representative spectrum of assets have declined more or less consistently since the middle of the 1980s. This is another way to say that the market price of those assets has tended to appreciate relative to the stream of their expected payoffs, discounted at the risk-free rate. Second, looking at higher-frequency movements around trends, I notice a turnaround in some financial series toward the end of the period. In particular, equity and credit financing has become more costly for firms to obtain, as the risk premia required for holding stocks and credit securities have recently bounced back from the lows achieved earlier. The upswing in the equity risk premium came first. The violent reversal in the credit risk premia is even more recent history.

Understanding these trends and co-movements is an important pre-condition for any inference we need to draw on the more recent turnarounds. So, I shall concentrate on low-frequency movements first, and come back to my interpretation of the turnarounds and the future at the end of my talk.

Why have required excess returns – risk premia – on, say, stocks trended down? Many explanations specific to the market for business capital are conceivable. One is that expectations of future cash-flows in the form of dividend payments might have consistently lagged behind ex post realisations, which in the end drive stock prices. [2] For example, the potential for sustained economic growth in excess of historical precedents, the availability of profitable investment projects beyond the frontier that was considered attainable ex ante might explain a fraction of the decline in required stock returns over a certain phase.

Why have term premia on bonds trended down? Again, specific factors affecting the market for safe financial investments have been cited. I have mentioned already that the rapid expansion of incomes in countries with high propensities to save meant that a large share of their increased demand for assets was directed to the risk-free financial liabilities of primary sovereign issuers, most prominently the US Treasury.

Similarly, trends in the market for homes and for private credit can be given explanations rooted in housing preferences and the evolution of default rates through time.

But there is one question which remains, beyond all these explanations. [3] They all are too specific to one market. As we see, declines in returns have been generalised. Estimated premia in the stock market in 2008 lie one third and two thirds below their values at the beginning of the 1980s, in the euro area and the US respectively. In the meantime, term premia on the bond market have lost three fourth of their estimated value at the middle of the 1990s in a seemingly relentless fall spanning the entire period for which we could compute them. The premium for investments in houses has followed a similar trend, despite a sharp reversion, in particular in the US in the most recent period. Finally, the cost of corporate borrowing in excess of a riskless rate [Figure 3], which remunerates credit risk, has also decreased significantly in both economies, although its trend is punctuated by significant oscillations in the opposite direction. Obviously we observe the same movements across the board.

Facts common to multiple markets suggest the existence of a common factor, something truly related to the size of the required premium for holding all types of risky assets. If the compensation for bearing risk is compressed in all markets, this must reflect that either the quantity of macroeconomic risk has gone down, or the price at which investors trade that risk has declined, or some combination of these two possibilities.

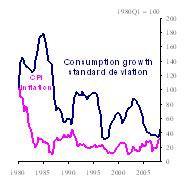

In these two further pictures [Figures 1b and 2b], the quantity of aggregate risk is proxied by the macroeconomic uncertainty introduced by the volatility of real per-capita consumption growth [– as measured by rolling standard deviations of per-capita real consumption growth –] and the level of inflation in the two economies. [4] Unfortunately, the price that markets attach to that quantity – agents’ risk aversion – is not directly observable or easily approximated by observable variables. I shall come back to this point later.

Why concentrate on consumption volatility as a proxy of real macroeconomic uncertainty? Because this is the privileged statistic of macroeconomic conditions in consumption-based asset pricing models, the standard tool of financial economics. In these models, it is the marginal utility of consumption and its variance that should help price real payoffs in different states of nature. [5] Why focus on inflation as an indicator of nominal uncertainty? If the level of inflation is correlated with its perceived variability, then the level of inflation should influence people’s views of the degree of uncertainty that surrounds their macroeconomic environments. If the nominal scale of the economy is more firmly secured, financial markets will likely reflect it in lower premia.

The drawn-out moderation in real macroeconomic volatilities – the Great Moderation – is a well-known fact. It has been persistent, as the pictures indicate, and broad, spreading beyond inflation and consumption to virtually all sectors and components of income, on a global scale, as many studies have demonstrated. [6] The tight correlation between the risk premia priced in various markets and movements in macroeconomic risk is less known, however. It is certainly of great interest to policymakers. [7]

It is a challenging piece of evidence for two reasons. Because causation can run both ways, from macroeconomic volatility – the quantum of non-diversifiable risk – to risk compensation in the financial markets, or from the market determination of the reward for risk – the market price of risk – back to the macroeconomic equilibrium. And because both chains of causation entail a blend of structural and contingent factors: factors that are likely to last and factors that are transient and bound to be reversed.

Therefore, in September 2008 a scholar, a forecaster, a policymaker looking back to the financial history of the last quarter of a century for clues about the proximate future evolutions faces two questions. First, what determined the compression of risk in virtually all markets: was it a reduction in aggregate risk, or was it a compression in the price for which markets trade and distribute that risk? Second, whatever the cause, did the compression of risk reflect permanent shifts in fundamental connections, or was it transient?

A lot – not least in terms of policy decisions – is conditional on a clear identification of these links, of these directions and their nature.

1.1 The quantum of risk: what is structural and what is transient?

Staring at the statistical association between premia and macroeconomic volatilities it would be tempting to draw a line of causation running from declining macroeconomic risk to falling premia. The decrease in macroeconomic uncertainty associated with the fall in the volatilities of consumption and inflation can arguably be expected to have resulted in a corresponding reduction in the uncertainty on future asset returns, thus leading to lower risk premia across the board. In the case of government bonds, for example, a decrease in macroeconomic volatility reduces the risk of unexpected future changes in interest rates – perhaps policy-induced – and removes one primary source of return uncertainty that investors in bonds have to hedge against in less tranquil times. [8] For corporate bonds and commercial paper, a decrease in the amplitude of business-cycle fluctuations should bring about, ceteris paribus, a lower probability of default, which, once again, can translate into lower credit risk premia. Analogous reasoning holds for stock and housing markets, with the fall in macroeconomic volatility translating into a decrease in the uncertainty about expected future returns, and therefore leading to lower risk premia.

However, even if one is prepared to entertain the possibility that the line of causation runs predominantly from macroeconomic conditions – fundamental macroeconomic stability – to asset price determination, the prospects for the evolution of market prices in the near future are vastly conditional on the nature of the macroeconomic moderation.

If one believes that the main reason for the observed decline in macroeconomic volatilities – and, indirectly, for low risk compensations and high prices in asset markets – is that policy regimes have become more stable, more predictable and confidence-inspiring, then prospects for market participants and policymakers alike will be brighter. We all know that the institutional roots of the Great Moderation are significant, as studies done at the ECB and elsewhere have shown. [9] We know that policy statutes – disciplining monetary policy and the fiscal authority – have been carefully crafted in many countries to make sure that stable policy conditions are put in place and are there to last. So, if all this is true, one could perhaps confidently extrapolate the moderate macroeconomic volatilities of the past into the future. And, in so doing, one would equally be reassured that the down-trends in risk compensation that we have observed for so long – beyond short-run ups and downs – would not be reversed in a sustained manner.

But the same line of causation could be less reassuring from another angle. The same studies that have found an important role for policies in the Great Moderation of the last two decades cannot certainly rule out that “good luck” might have exerted a reinforcing influence. More moderate exogenous shocks might have contributed – more or less accidentally – to smoothing economic fluctuations. In the terms of our picture, this would be equivalent to say that the moderation in some non-policy factor driving activity might have been responsible for the fall in inflation and consumption variability.

To the extent that this interpretation has some merit, a less fortunate string of shocks could always bring more ample swings in economic conditions – looking forward – than we have grown accustomed to from past experience. And this could entail repercussions for the valuation of investment risk in various financial markets. In this case a return to historical valuations for risk would imply large negative returns for a possibly extended period of time.

1.2 The price of risk: what is structural and what is transient?

It is important to understand that the close co-movements that appear when comparing trends in premia with trends in macro-volatilities are not inconsistent with an alternative, inverse pattern of causation: one predominantly running from financial market prices to the macro-economy.

Exogenous changes in financial markets may have caused an original fall in risk premia. Since asset prices provide signals for profitable investment opportunities, affect the wealth of households, and influence the cost of capital to firms and households, a compression of risk premia in the markets for capital and credit may have put the economy on a different expansion path where incomes grow faster and are less uncertain.

But, again, independent changes in financial markets can be of a structural or more transient nature.

I shall start with structural factors. A major source of structural evolution in financial markets over the last twenty years, one that is difficult to overlook and that is likely to last, comes under the encompassing label of increased financial market participation. Institutional investors, such as pension and mutual funds, hedge funds, and more recently sovereign wealth funds, have been playing an increasingly important role in many asset markets. The informed, active trading of these investors has increased market liquidity and led to a reduction in transactions costs. Deeper and less expensive markets have meant that the typical investor – once holding a poorly diversified portfolio with skewed returns – is now better diversified and thus more risk-tolerant. At the same time, the introduction of non-redundant and previously non-existing assets and liabilities has provided a further encouragement for investors and financial intermediaries to transform and transfer risk. The enhanced availability of these new instruments has increased the accessibility and availability of credit to the private sector. I will return to the toxic side of these developments in a minute. Here, as in many studies, I note that an increase in participation has the potential to decrease the required risk premium on a wide spectrum of assets, because it spreads market risk over a broader population. [10]

For a given amount of macroeconomic risk – a given quantum of macro-volatility – increased participation can cut the price of risk. And a lower price of risk that is due to a structural break in market participation rates is more likely to persist.

But transient factors in financial markets might have been at work as well. For a given quantum of macro-volatility and a given fundamental price of risk, markets can at times under-appreciate the former and under-price the latter. Risk aversion can fluctuate around a fundamental value which is determined by long-lasting evolutions in financial market infrastructures and financial market participation. And these more contingent fluctuations in risk aversion can be slow to re-absorb. Changes in risk aversion can at times look a lot like “bubbles”. But swings in risk aversion that will eventually revert back to some sort of equilibrium are, in my view, the manifestation of a phenomenon – more general than “bubbles” – which has been rationalised and modelled in various ways. [11] The important point is not so much to understand what causes such fluctuations in risk preferences – whether explosive expectations [12] or habit formation in consumption – but that they are ephemeral and, once they take off, they tend to fall back to ground.

Occasional waves of higher risk tolerance in financial markets can expand the supply of external finance for the productive sector and for government. And this can make previously unprofitable investment programs look attractive, which can boost growth. But, unlike more structural shifts in financial market infrastructures, occasional turns in risk tolerance are just that: occasional.

Reversion to some sort of steady values for risk appetite can undo established market trends and give rise to a prolonged period of strains in market valuations.

2. New channels of interaction

Varying risk premia blur the fundamental connection between asset prices and real economic decisions. This has been studied extensively and the evidence that I have provided thus far is, after all, but one variation on a traditional theme in financial economics: the risk premium puzzle.

But today risk pricing and macroeconomic performance can make contact in ways that are novel and still little known. Here I would like to draw your attention to the increased participation of financial investors – especially hedge funds and institutional investors – in commodity markets. [13] This trend has accompanied the spectacular boom in commodity prices over the last few years and has complicated the interpretation of the fundamental drivers of prices in those markets in various phases.

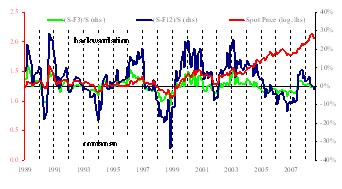

We can take the oil futures markets as an example. Futures contracts are agreements to buy or sell a specified quantity of a commodity at a future date, at a price agreed upon when entering the contract, the futures price. However, in regulated exchanges [such as NYMEX or ICE] these contracts are traded chiefly for hedging risk on price changes rather than for arranging physical delivery of oil. [14] Traditionally, these markets have been characterised, more frequently than not, by a market constellation of prices known as ‘backwardation’. This indicates a situation in which futures prices are below the current spot price [ see Figure 4]. [15] To understand what this means, note that both producers and consumers of oil are normally interested in hedging the risk of fluctuations in the future spot price of oil – which is unknown today. But, since oil production and supply is concentrated among far fewer participants than total consumption among consumers, suppliers are more likely to factor the risk of future price fluctuations into their economic decisions to a larger extent than any single buyer. This strengthens the incentive for suppliers to hedge against adverse fluctuations in spot prices. Traditionally, the market for oil futures has been a “sellers’ market.” And sellers have been on average happy to pay a premium to market traders willing to buy a futures contract and take upon themselves the risk of future spot price declines. “Backwardation” means that buyers as a whole normally agree to provide this insurance if they can expect to earn a positive premium on top of the expected change in the future price of oil. [16] Assuming that the best predictor of the spot price in the future is the current spot price, the spread between the current spot price and the futures price reflects the remuneration for the risk that buyers as a whole accept to bear. [17]

Over the last two decades when backwardation has been the norm, the risk premium paid by hedgers to financial investors has been relatively stable, moving predictably with the spot price of oil [Figure 4]. [18] More recently, since 2005, this relationship between the risk premium and the spot price of oil appears to have changed and risk premia paid by hedgers have been shrinking to become even negative between early 2005 and 2007. [19] This is clear from the evolution over time of the futures price curve [for Brent oil price], on which the ECB oil price projections are based. The curve clearly moved from a downward slope to an upward tilt around the same time and maintained the increasing tilt at least until the middle of 2007 [ Figure 5].

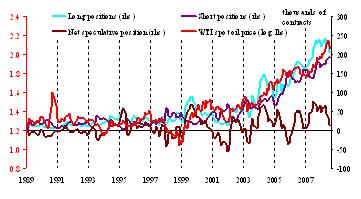

This atypical compression – and inversion – of the risk premia paid in the oil futures market has gone hand in hand with an appreciable change in the structure of these markets, with a growing involvement of non-commercial participants. The change in the composition of the market has been made evident by the emergence of a new net positive speculative position [Figure 6]. It seems as though the market for oil futures, traditionally dominated by hedging sellers, had at times become a “buyers’ market.”

How are these developments to be interpreted? What is the direction of influence between fundamental trends in the real economy and the pricing of financial risk? A fundamentals-driven interpretation has it that increasing futures prices indeed signal a fundamental break in spot price expectations: which traditionally had been “mean-reverting” and might have become persistently bullish, reflecting a perceived break in the anticipated imbalances between oil demand and oil production on a global scale. But observers focusing on the change in the balance between short and long positions in the market have pointed to the possibility that futures prices – determined on a market in which buyers are increasingly motivated by a search for financial yield rather than the incentive to hedge – might have been contributing in certain market phases to movements in the spot price.

Have financial investors played a stabilising or a destabilizing role at a time of booming commodity prices and heightened uncertainty about their long-term fundamentals? According to a benign view, ‘financial investors’ have expanded liquidity in commodity markets, and have made the market more efficient in processing information, thus improving price discovery at a time of greater uncertainty about fundamentals. New financial actors such as highly leveraged funds and institutional investors may have contributed to lowering spreads and the associated risk premia in commodity futures markets by spreading their own portfolio risk more widely. In this sense, they may even have strengthened the traditional insurance role of futures markets. In addition, financial investors may have helped bring forward price increases that would have occurred nonetheless. This may have provided a signal to both consumers and producers that they needed to start adjusting their consumption and investment plans before the economy hits the physical constraints of oil supply. In this sense, some volatility today might have been the price to pay to avoid even higher volatility in the future.

But, according to an opposite interpretation, financial investors operating systematically on the futures market might have reduced the risk and the cost faced by sellers who want to accumulate inventories, or possibly delay production to gain from steep anticipated price trends. In this way they might have exacerbated changes in prices and inventories due to predicted changes in fundamentals. They might have sent noisier and potentially distorted signals to producers and consumers. [20]

If this seems to me a reasonable conjecture, I admit, though, that existing evidence does not provide uncontroversial support to the notion that non-commercial investors in futures markets have been systematically playing a significant role in pushing spot prices out of their fundamental equilibrium.

3. Interpreting the present situation

Since August 2007, markets have become increasingly discriminating with regard to the risks posed by the real investment projects underlying a wide range of securitised credit. This new attitude is reflected in the large rebounds in risk premia that I have noted in my charts. Spreads on financial institution debt, in particular, have widened in the euro area and in the US reflecting uncertainty over the extent of future credit write-offs, the full recognition of off-balance-sheet commitments, and future earnings capacity. The wide perception in the markets is that financial institutions face difficulties in maintaining earnings due to falling credit quality and declining fee income in a macro-economic environment already taxed by sharp rises in real production costs. As intermediaries tend to economise on capital, assets are being sold and lending conditions have tightened. As I have shown in Figure 3, the correction in the appraisal of risk has thus been broad-based, and spreads on funding costs for corporates have stuck to levels that had not been on market records for a long period of time.

My conjecture is that the recent corrections and retrenchments in financial markets bring two lessons and leave much to be learned from future analysis and experience. I start from the two lessons.

First, as has often happened in the past, non-fundamental market dynamics have grown out of fundamentals and the feed-back loops that these have created. As I said already, increased financial market participation has set a new secular trend toward a lower price of risk sustained by long-term financial deepening. Financial deepening, in turn, has initially responded to a real demand for a more efficient sharing of risk. More effective risk sharing has meant better mechanisms through which producers and ultimate savers can hedge open positions arising from their real transactions. As a side-effect, this process – generalised to a wide range of markets – has brought sustained capital gains to an expanding number of beneficiaries. This, in turn, has improved incomes and the economic outlook. And the process has been feeding and reinforcing itself.

Second lesson: “good health is always a precarious situation that does not presage anything good.” At some point in the maturing process, brighter prospects have meant under-assessment of the macroeconomic risk and under-pricing of the unit quantity of risk. Financial markets have ceased to facilitate the dispersion of the risk that is intrinsic to the underlying economic activities, and they have developed into formidable risk multipliers. The new structured financial products that grew exponentially in the ten years leading up to the recent disorders in financial markets, by pooling and repackaging income streams of different quality, gave the false impression that the benefits of diversification would reduce the risks inherent in the underlying assets. But the leverage embedded in those products meant that end-investors were in fact exposed to a quantum of risk that could outstrip – rather than mitigate – that implied by the underlying pool of assets. Excessive leverage was the mechanism which – at some point – turned an efficient process of risk diffusion into a dangerous spiral of risk amplification and concentration.

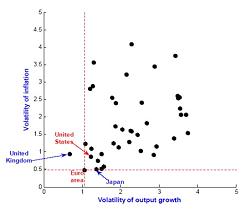

Third: stable institutions and firm monetary policy frameworks are needed more than ever in times of turbulence: financial stability is no substitute to price stability. The latter is a precondition to the former. As I said, a significant part of the decline in macroeconomic uncertainty is no windfall for modern societies: it is the fair and expected reward for institutional reform. In continental Europe, this reform has been induced largely by the need to converge to sound macroeconomic policies as signalled, in particular, by the best macroeconomic regimes that were available in the Continent. The process has been successful, both historically – comparing performances before and after monetary union [Figure 1b] – and in cross-section. This figure [Figure 7] establishes a comparison between macroeconomic volatilities in the euro area and elsewhere since 1999: a comprehensive cross section of international macroeconomic outcomes. Despite recent shocks, the euro area countries have compressed aggregate risk relative to their past, and have done it beyond the standards that are set by other countries. Stable and transparent monetary institutions have helped the economy before – remember the stock market collapse of the early years of this decade – and will help this time.

But – here suggestions for further reflection and analysis start – to what extent have stable macroeconomic frameworks genuinely squeezed risks out of the system? And to what extent have they encouraged over-confidence and complacency? We saw that complacency played a role in the under-pricing of risk in a certain market phase. But the remaining question is whether the relaxation in financial prudence could have been triggered by false expectations of a perennially smooth economic environment that policymakers could have avoided in words and deeds.

Developments in financial markets have largely coincided with pressures on the real costs of commodities which – in terms of intensity and persistence – have been largely unprecedented. As I tried to argue, it is not clear whether the inversion of the oil futures curve – with futures prices occasionally increasing above spot prices – should be taken to signal a permanent inversion of spot price expectations, presaging a long period of further appreciations in the real price of energy. Or, simply, it should be understood as yet another reflection of a varying risk premium signalling a wedge between asset prices and fundamentals.

Today more than ever before, efforts – by scholars and central banks alike – to connect market returns and risk pricing to a fuller range of macroeconomic phenomena have high potential pay-offs. The challenge, in the end, is to build models that can match asset pricing facts, while at the same time maintaining – if not improving on – the existing business cycle models’ ability to account for quantity fluctuations. This is no small challenge. These models would need to match the price of risk and the relative volatilities of consumption, output and investment. By doing so, they would offer instruments for evaluating the predictability of asset returns – and their cross-section – based on assumptions about the evolution of the real economy.

They would allow interpreting the drawn-out declines in risk appreciation that have spanned more than two decades. Most importantly, they would be suitable tools to measure the exact proportion in which the more recent changes in risk premia reflect stable breaks in the reward for risk, or are products of transient market whims. They would help disentangle the effects on commodity prices of fundamental trends in oil demand – which are likely to be sustained and thus most relevant for policy – from the swinging influences of new financial strategies.

Ideally, these new models would offer ways to simulate and stress-test situations of unquantifiable – Knightian – uncertainly, where past correlations collapse and perverse expectations determine new dynamics.

4. Implications for financial participants

But, as I speak, we still have a lot of work to elucidate these interactions.

Financial participants and policymakers have to rely on robust behavioural rules that can minimise the chance that business strategies and policy decisions might be based on a misguided model or an over-optimistic representation of economic reality. I will start with two fundamental principles that should govern the business model of financial operators and protect them from the hazards of excessive risk taking. I will then turn to monetary policy.

First, financial participation and financial sophistication find their limit in complexity. The recent experience has taught us that increasing complexity of financial instruments can undermine the benefits of financial innovation. Savers become more risk averse – sometimes through abrupt retractions from market trading – if faced with increasing difficulties in evaluating the risk to which they are exposed. The recent market strains started to pose challenges to the macro-economy at large when investors sought clarity about the quality of specific assets supporting investment securities, and shed those whose risk they could not easily assess. And a primary source of losses for financial institutions came from the concentrated exposures that were implicit in the warehousing, structuring and trading of complex credit derivatives. Complexity prevented them from fully appreciating the possibility that the losses in the underlying assets could – in distressed market conditions – reach levels which would impair the value of the super-senior tranches that they had retained in their balance sheets.

Second, the management and the valuation of risk at the level of business units have become critical activities. As I said before, expanded financial participation can cut the share of risk that each participant shoulders at each point in time. But the dark side of this phenomenon is that it also provides an encouragement for financial services organisations to expand the overall amount of risk that is traded. And it weakens market participants’ anti-bodies against excessive individual exposure and risk taking. There is evidence that the financial firms that have performed better since the turmoil began a year ago are those in which management had established rigorous internal processes and discipline in the valuation of risk. Those are firms that had not exclusively relied on external views of credit risk – from rating agencies or pricing services – but had also developed in-house expertise to conduct independent assessments of the most critical positions. They had established stronger internal checks over individual business lines to control activities that had the potential to lead to significant balance sheet growth or unexpected reductions in capital. The sophistication of their risk measurement processes had kept pace with increasing risk taking. The quantitative methodologies employed were varied – notional limits to risk assumption, value-at-risk indicators, stress tests and forward-looking scenario analysis – and flexible, so that management could quickly vary assumptions about the scale of shocks or the degree of market volatility and the pattern of asset correlations in difficult market conditions. These firms had resisted the tendency – which becomes widespread in times when risks seem well-distributed and traders well-diversified – to a dilution of the incentive to exercise prudence.

Controlling the primary sources of excessive risk taking is within the control of major financial participants. It is critical that internal processes and practices be deployed that can curb the tendency to expand business aggressively in times of greater propensity to risk taking, to a point beyond the capacity of the relevant control infrastructures.

Supervisory oversight can and will support efforts in this direction. Among other supporting measures, strengthened prudential oversight of capital, liquidity and risk management is of the essence to ensure an appropriate capital treatment and disclosure of on and off-balance exposures and that liquidity buffers correspond to the liquidity risks incurred. Supervisors and regulators will communicate early to firms’ boards their risk management concerns and the need to take responsive action.

5. Implications for monetary policy

The swinging and unpredictable interactions between the markets and real economic decisions are unlikely to have long-lasting and severe consequences for the macro-economy as long as monetary policy maintains a clear sense of direction.

I already highlighted the role that new monetary policy frameworks have played in the transition to a new macroeconomic regime, in which incomes, consumption and other measures of economic welfare follow a steadier course. As I tried to argue, the interpretation of the link between the reduction in macroeconomic uncertainty – the Great Moderation – and the pricing of that uncertainty in the markets poses many unresolved issues. But very few observers and scholars would object that central banks’ commitment to keeping inflation low and stable, their improved communication about their price stability objectives and their acting on those objectives by the force of deeds, has importantly contributed to the reduction in macroeconomic risk that we find in the data. They would also agree that if aggregate – un-diversifiable – risk diminishes, this ought to be reflected in the premia that financial markets pay for risk taking. That fraction of reduced risk compensations is a stable acquisition of modern economies. The complement to that fraction – what is due to excessive financial sophistication, abnormal risk tolerance and shortcomings in risk management; and what is due to the persistence of international imbalances and the steady appreciation of commodities – will pass.

At this stage, let me make three remarks.

First, we have exercised an ongoing warning function, whenever the amount and the price of risk traded in financial markets had departed from the trends that appeared justified by lasting changes in macroeconomic fundamentals. Our communication on the financial imbalances that were being created in the over-confident market conditions that prevailed until the summer of 2007 has been vindicated ex post. Starting from last summer, financial markets have finally initiated a process of re-pricing of risk to more appropriate levels, and to pay more attention to the quality of the assets they invest in, although this process has been significantly less orderly than we would have hoped. Since risk premia across a wide spectrum of assets had fallen to excessively low levels, their return to more appropriate values—and the accompanying process of financial de-leveraging—is to be regarded as a necessary development. Under this respect, the most appropriate policy response is therefore to allow such process to take place in an as orderly way as possible, playing a supporting role whenever medium-term downside risk to price stability might emerge along the way.

Second, we have been crystal-clear since the beginning of the financial turbulence that we would make a strict separation between the monetary policy stance – which is designed exclusively to deliver price stability in the medium term in an exceptionally difficult period – and the implementation of this monetary policy through the Eurosystem credit operations. These operations were designed with a view to maintaining the short-term rates close to our policy rates within an environment of turbulent money markets. This concept has been well understood by market participants and has preserved the integrity and the credibility of our monetary policy. It has also facilitated our fundamental goal to preserve a firm anchoring of inflation expectations in line with our definition of price stability.

Third, let me concentrate on inflation expectations in an environment of sustained supply-side shocks. We need to consider that the sequence of shocks to commodity prices that we have faced in the past five years confronts us with a difficult identification problem. Supply-side shocks that hit in one direction for such a prolonged period of time can become engrained in inflation expectations. If – and when – this happens, then these shocks change their nature. If they de-stabilise expectations, they become more similar to demand shocks. A demand shock calls for a shorter policy horizon.

Our policy horizon is the medium term, and the medium term should be taken to be at least as long as the average transmission lag for policy actions. While facing rises in commodity prices, the policy horizon could theoretically be more extended. But, the circumstances that I just described are not typical and the risk that a repeated sequence of supply-side shocks might turn into a demand disturbance with long-lasting implications for price stability has made our horizon shorter. It has made it closer to the average transmission lag.

6. Concluding remarks

As I pointed out in my opening remarks, these are testing times. The financial turbulence that started last summer, and the increases in commodity prices of the last few years, conjured to create a very challenging environment, in which central banks have to simultaneously face off the fragilities of the financial fabric and the inflationary pressures originating from global commodity markets. It is precisely during such difficult times that the benefits of a solid monetary framework oriented to price stability become apparent. Our framework—with a strong mandate for price stability, a focus on a firm anchoring of inflation expectations, and a crucial role assigned to a monetary aggregates—is, under this respect, ideally suited to the challenges we are currently facing, as it encodes the lessons of the central banks which, during the 1970s, successfully ‘opted out’ of the Great Inflation. This framework, coupled with our absolute resolve to avoid repeating the mistakes of the 1970s, will guarantee price stability, thus contributing to economic growth and job creation in the euro area.

Thank you for your attention.

Figure 1: Euro area, Risk premia and Macroeconomic Risk

| (1a) Equity, bond, housing risk premia | (1b) Consumption growth volatility and HICP inflation |

|---|---|

|

|

| Source: ECB, Datastream. Note: The equity (Total EMU stock market) and the housing (residential property prices) risk premia are calculated based on the assumption of a very long-term risk-free nominal interest rate and a very long-term growth rate of payouts. The term premium (10 year bonds) is calculated based on an affine term structure model with survey data similar to Kim and Orphanides (2005). | Source: ECB, Eurostat, European Commission. Note: The consumption growth standard deviation is computed as the 5-year moving standard deviation of per capita consumption growth. HICP inflation is the year-on-year percent change in the HICP. |

Figure 2: US, Risk premia and Macroeconomic Risk

| (2a) Equity, bond, housing risk premia | (2b) Consumption growth volatility and CPI inflation |

|---|---|

|

|

| Source: ECB, Kim and Wright (2005), Davis et al. (2007), Global Financial Data, Datastream, Freddie Mac and Bureau of Labor Statistics Note: The equity (S&P 500) and the housing (owner-occupied houses) risk premia are calculated based on the assumption of a very long-term risk-free nominal interest rate and a very long-term growth rate of payouts. The term premium (10 year bonds) is calculated based on an affine term-structure model (Kim and Wright, 2005). | Source: ECB, St. Louis FRED database Note: The consumption growth standard deviation is computed as the 5-year moving standard deviation of per capita consumption growth. CPI inflation is the year-on-year percent change in the CPI-U. |

Figure 3: Credit spreads in the euro area and US

|

|---|

| Source: ECB, St. Louis FRED database, Merrill Lynch Note: Spreads over AAA corporate bond yield. |

Figure 4: Futures spreads on NYMEX & oil spot price (WTI)

|

| Source: Bloomberg. Note: Futures spreads (right hand scale) are defined as the difference between the current spot price and the futures prices at different maturities, scaled by the current spot price. Prices are those traded in NYMEX and refers to West Texas Intermediate (WTI). The spot oil price is in log (left hand scale). Monthly observations refer to the last trading day of each month. |

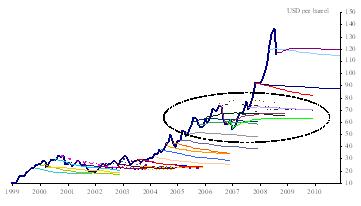

Figure 5: Futures curve for Brent oil price

|

| Source: IMF, Bloomberg, and ECB calculations. Note: The futures price curves reflect the path implied by futures markets in the two-week period ending on the cut-off date of the Eurosystem/ECB staff macroeconomic projections. |

Figure 6: Number of positions by non-commercial participants (NYMEX) & WTI oil price

|

| Source: Bloomberg. Note: Number of contracts in thousands (3-month moving average). The oil price is in logs. |

Figure 7: Macroeconomic volatility in the euro area and elsewhere since January 1999

|

| Source: ECB Calculations. Note: Standard deviations of annual CPI inflation and output growth since January 1999. |

References

Alquist, R. and L. Kilian (2008), “What do we learn from the price of crude oil futures?’, unpublished paper, University of Michigan.

Benati, L. and P. Surico (2008), ‘VAR Analysis and the Great Moderation’, forthcoming in American Economic Review.

Campbell, J. and J. Cochrane (1999), ‘By Force of Habit: A Consumption-based Explanation of Aggregate Stock-Market Behaviour’, Journal of Political Economy 107: 205-251.

Campbell, J. and R. Shiller (2003), ‘Valuation Ratios and Long-run Stock Market Outlook: An Update’, in Advances in Behavioural Finance, Volume II, edited by N. Barberis and R. Thaler, Russel Sage Foundation, New York, NY.

Davis, M., A. Lehnert and R. Martin (2007), ‘The Rent-Price Ratio for the Aggregate Stock of Owner-Occupied Housing’, mimeo, Federal Reserve Board of Governors.

Domanski, D. and A. Heath (2007), ‘Financial Investors and Commodity Markets’, BIS Quarterly Review (March).

Gorton, G. and K. G. Rouwenhorst (2004), ‘Facts and Fantasies about Commodity Prices’, NBER Working Paper No. 10595.

Jagannathan, R., E.R. McGrattan, and A. Scherbina (2000), ‘The Declining U.S. Equity Premium’, Federal Reserve Bank of Minneapolis Quarterly Review 24(4), Fall 2000: 3-19.

Kim, D. and A. Orphanides (2005), ‘Term structure estimation with survey data on interest rate forecasts’, FED Finance and Economics Discussion Series 2005-48.

Kim, D. and J. Wright (2005), ‘An Arbitrage-Free Three-Factor Term-structure Model and the Recent Behavior of Long-Term Yields and Distant-Horizon Forward Rates’, FED Finance and Economics Discussion Series 2005-33.

Lettau, M., S.C. Ludvigson, and J.A. Wachter (2008), ‘The Declining Equity Premium: What Role Does Macroeconomic Risk Play?’, Review of Financial Studies 21(4): 1653-1687.

Pagano, P. and M. Pisani (2006), ‘Risk-adjusted forecasts of oil prices’, Temi di discussione no. 585, Bank of Italy.

Plosser, C. I. (2007), ‘What Can We Expect from the Yield Curve?’, speech given by Charles I. Plosser, President and Chief Executive Officer Federal Reserve Bank of Philadelphia to the New Jersey Bankers Annual Convention, Palm Beach, Florida, March 23, 2007

Rudebusch, G., E. Swanson and T. Wu (2006), ‘The Bond Yield Conundrum from a Macro-Finance Perspective’ Monetary and Economic Studies, Institute for Monetary and Economic Studies, Bank of Japan, vol. 24(S1), pages 83-109, December.

Sharpe, S. (1999), ‘Stock prices, Expected Returns and Inflation’, Board of Governors of the Federal Reserve System FEDS Paper, 99-02.

Stock, J. and M. Watson (2002), ‘Has the Business Cycle Changed and Why?’, in NBER Macroeconomics Annual 2002, Cambridge, Mass., The MIT Press.

-

[1] Defining the stream of cash-flows earned by the asset by {dt}t=0...∞, the market price at time t of an asset with an extremely long maturity, pt, satisfies the following identity: pt = ∑j=1... ∞ (1+ rt + πt)-j Et dt+j, where Et is the expectations operator at time t. The financial factor that is used to discount the expected stream of payouts, rt + πt, has two components: a risk-free rate, rt, which could be earned on a competing asset with certain returns, and an excess rate of return, πt, which remunerates the investor for the added risk that she is taking on. I shall refer to the latter factor, interchangeably, as excess return or risk premium.

-

[2] Referring to the formula in the previous footnote, and interpreting {dt}t=0...∞ as the actual (ex post) stream of dividend payments, systematic underprediction of the dividend stream looking forward from any given vantage point t can result in an underestimation of the return that can be expected, at t, from holding the stock at the current price pt because the market price grows at the growth rate of the actual dividend payments.

-

[3] In fact there are more problems. First, explaining low equity risk premia with systematic under-prediction of income streams has limited explanatory power. If anything, the scant evidence available on earnings expectations point in the opposite direction. Sharpe (1999), for example, finds that in the period between 1994 and the end of the century forecasts of two-year nominal earnings growth were high and stable (between 10% and 15%), even though realised two-year earnings growth were declining. It should also be noted that higher growth in realised payoffs, per se, is not sufficient to account for price movements over the entire sample, because dividend-to-price and earning-to-price ratios have themselves trended down. The secular fall in the dividend-to-price and earnings-to-price ratios is actually the fact that needs to be explained in the first place. See, among many others, Jagannathan, McGrattan and Scherbina (2000). Second, concerning low term premia, foreign official purchases of US bonds – by the monetary authorities of countries which follow a stable exchange rate policy vis-à-vis the US dollar – was found to have played little or no role as a factor contributing to low long-term interest rates in a study of the interest rate conundrum. See Rudebusch, Swanson and Wu (2006).

-

[4] The level of inflation is found to be correlated with its variability, which in turn should influence people’s perceptions of the degree of uncertainty that surrounds their macroeconomic environments.

-

[5] In many standard asset-pricing models with complete markets, the risk premium, or excess return, paid by an asset with uncertain payoffs is proportional to the volatility of consumption, with a risk aversion parameter as the constant of proportionality. In these models, aggregate consumption volatility stands for the quantity of risk, while the parameter scaling agents’ risk aversion stands for the price of risk. A crucial subsidiary assumption behind this logic is that all wealth – including human capital – is tradable, so that the aggregate return can be interpreted as the gross return to an asset that represents a claim to aggregate consumption.

-

[6] Stock and Watson (2002), among others, show that the decline in volatility appears in a large number of macroeconomic time series: employment growth, consumption growth, inflation and sectoral output growth, as well as in GDP growth. The decline is not confined to the US economy, but is well visible in a vast array of economies, both industrialised and developing, with few exceptions.

-

[7] A correlation between different indicators of equity valuations and consumption volatility for a set of eleven industrialised countries has been noted before. See, for example, Lettau, Ludvigson and Wachter (2008). But Figures 1 and 2 document that evidence of this type of correlation is more pervasive than studied in their paper.

-

[8] A detailed discussion along these lines of the impact of a fall in the volatility of inflation and output growth on the bond term premium can be found, e.g., in Plosser (2007).

-

[9] Benati and Surico (2008) finds that the role of stabilising monetary policy can go some way toward explaining the Great Moderation.

-

[10] The emergence and growth of new financial intermediaries can have further and deeper causes. For example, the more recent, accelerated integration of emerging markets into the global economy may have led to an increase in global savings and, as a result, to a growing demand for financial services and new financial operators. Also, the achievements of peak-savings years by the baby-boom generation might have expanded the pool of resources that need to be intermediated by specialised pension funds. In fact, the abundance of global savings – whether induced by the globalisation of economic processes or by the aging of a large share of the world population – is indeed one of the explanations advanced for the exceptionally low bond yields recently observed in the U.S. and, to a lesser extent, also in the Euro area.

-

[11] For example, models in which investors’ preferences display habit formation – the argument of utility is not the absolute level of consumption but the level of consumption relative to some “normal” level – can generate time-varying risk tolerance. Agents are more risk averse when current consumption is around the level that they consider “normal” based on their past income/consumption history. In these circumstances – which indeed should apply in normal times – only a small fraction of consumption is available as a surplus to generate utility, and even small shocks to consumption can have a large effect on this surplus. Therefore, investors are extremely risk averse. A positive shock to income can cause actual consumption to exceed its perceived “normal” by a wide margin and for a prolonged period of time. This increases agents’ risk appetite because now the consumption surplus is larger. Campbell and Cochrane (1999) prove that the (equity) risk premium can fluctuate due to this mechanism.

-

[12] Within the cash-flow-discount model for asset pricing that is expounded in footnote 2, seemingly explosive price dynamics can be generated by a sequence of negative innovations to the risk premium, πt.

-

[13] See, for example, Domanski and Heath (2007).

-

[14] Although physical delivery of oil may occur, this in reality occurs rather rarely. Contracts are instead liquidated before expiration usually leading to exchange of cash among market participants. So, for example, while an airline normally buys jet fuel through its usual physical supplier, it can purchase a futures contract to hedge possible price increase over the subsequent months. If the price actually rises, the gain from liquidating the futures contract towards expiration will offset the loss from the greater cost of fuel.

-

[15] The opposite situation in which the term structure of futures prices is upward sloping is known in traders’ jargon as “contango”, and has traditionally occurred less frequently than “backwardation”.

-

[16] Some financial participants may be enticed to buy or sell futures contracts by different views on the future oil price than the market. But on average financial participants are net buyers and assuming that they are on average no better than sellers in predicting the future spot price, they will need a discount over the price expected at the expiration of the futures contract to be motivated to purchase it.

-

[17] This risk premium is the mirror image of what sellers as a group are willing to give up for the benefits of holding physical inventories of oil, which have the important role of ensuring the continuation of production and sale in the face of potential disruption in the oil supply chain. In jargon inventories provide a “convenience yield”, which in the oil market can be quite sizeable. The convenience yield is normally inversely related to the deviation of inventories from their desired size.

-

[18] This pattern presumably reflected the belief of market participants in a stable long-run price of oil to which the spot price was expected to revert eventually.

-

[19] Here we focus on a measure of the risk premium (or roll return) earned by buyers of futures based on the assumption that the best predictor of the future spot oil price is today spot price. This allows an immediate interpretation of the observed spreads over the spot price at which futures contracts are traded. And, most importantly, over longer samples it is found to be the most accurate predictor (Alquist and Kilian, 2008). However, other measures of the risk premium in oil futures are also conceivable and used in practise (in particular in central banks’ forecasts). For example, Pagano and Pisani (2006) regress the ex-post realised risk premium on a constant and the degree of variable capacity utilisation in US manufacturing (a proxy for the state of the business cycle), taking the fitted value as their measure of risk premium.

-

[20] The accumulation of inventories may have sustained increasing spot prices from 2003 till the middle of 2007. Yet the spot price has continued to rise since. The fall in inventories may of course simply be due to tighter fundamentals.

Europejski Bank Centralny

Dyrekcja Generalna ds. Komunikacji

- Sonnemannstrasse 20

- 60314 Frankfurt am Main, Niemcy

- +49 69 1344 7455

- media@ecb.europa.eu

Przedruk dozwolony pod warunkiem podania źródła.

Kontakt z mediami